What happened

本期播客讨论了Is the AI bubble about to burst, and what’s driving analyst jitters?相关话题,为您带来深度分析和见解。

Concerns over a potential bursting of the artificial intelligence bubble have resurfaced with intensity, as US technology stocks recently faced their sharpest pullback since the Trump tariff-induced sell-off last April. Such movements have clear consequences when the sector is so pivotal for the markets.

AI-related stocks have contributed to roughly 75% of the S&P 500’s returns, 80% of earnings growth, and 90% of capital spending growth since the launch of OpenAI’s ChatGPT in November 2022. The so-called “Magnificent Seven” — Nvidia, Microsoft, Apple, Alphabet, Amazon, Meta Platforms, and Tesla — now collectively command a market capitalisation greater than the Chinese economy.

Nvidia alone is worth more than Japan, the world's third largest economy. But first: what defines a financial bubble? Can we really say that the current AI boom qualifies as a bubble? What does this phase of market euphoria have in common with the early 2000s — and more importantly, what sets it apart?

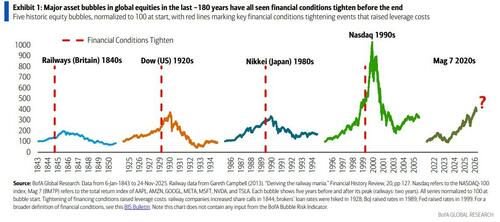

Are current trends echoing the dot-com bubble? The investment community remains starkly divided over whether we are witnessing a speculative bubble in the AI industry. While some observers draw uncomfortable parallels with the dot-com crash of the early 2000s, others argue that the current AI revolution is underpinned by genuine, transformative economic fundamentals.

UBS chief global equity strategist Andrew Garthwaite argues that the AI boom checks all the boxes for a classic bubble. He highlights several familiar patterns. Firstly, a pervasive “buy the dip” mentality, when investors flock to an asset when its price falls. Secondly, an investor belief that “this time must be different” due to revolutionary technology.

Thirdly, increased retail participation, along with loose monetary conditions and a backdrop of stagnant earnings outside of the top ten US companies. Garthwaite notes that 21% of US households now own individual stocks, with that number rising to 33% including investment funds. Meanwhile, earnings growth is largely confined to the tech giants.

“Today, outside the top ten companies in the US, 12-month forward earnings per share growth is close to zero,” he said. However, others caution against simplistic comparisons with the dot-com era. Goldman Sachs equity analyst Peter Oppenheimer points out, that unlike speculative companies of the early 2000s, today’s AI giants are delivering real profits.

“While AI stock prices have appreciated strongly, this has been matched by sustained earnings growth, not mere speculation,” said Oppenheimer. The current scenario of expensive equity valuations, Oppenheimer highlights, is less about speculative mania and more a reflection of broader macroeconomic conditions: low interest rates, high global savings, and a long economic cycle boosting risk assets.

A key distinction between the current AI boom and the dot-com bubble of the late 1990s lies in valuations. Goldman Sachs indicates that the median 24-month forward price-to-earnings (P/E) ratio for today’s ‘Magnificent Seven’ stands at 27 times earnings. This is nearly half the median valuation of the top tech stocks during the 2000 bubble, when companies like Cisco Systems, IBM, Oracle, Lucent Technologies, traded at eye-watering P/E multiples.

Not an AI bubble, but a power bottleneck? Whether or not the AI boom will end in a bubble remains an open question that continues to divide the investment community. However, beyond speculation about future valuations, a more grounded and pressing issue is emerging. Until now, much of the conversation around AI has focused on demand— on whether AI products and services meet real customer needs.

But a new perspective is gaining traction: demand is not the problem. In fact, it is so strong that the industry’s ability to supply the necessary computing power and physical capacity is struggling to keep up. According to Jordi Visser, head of AI Macro Nexus Research at 22V Research, the AI industry is facing a serious supply-side challenge — particularly in terms of the energy and infrastructure required to support its growth.

“This is not the dot-com bubble, because demand is massively outpacing supply,” Visser said in a recent YouTube video. According to Visser, “the next AI investment phase will not be defined by who can spend the most, but by who can execute through constraint”. He cited CoreWeave’s recent earnings call as a watershed moment.

Despite surging demand, the AI-cloud company’s revenue backlog nearly doubled quarter-over-quarter to $55.6 billion (€47.98bn), CoreWeave slashed its 2025 capital expenditure guidance by up to 40%, citing delayed power infrastructure delivery. Oracle, too, is experiencing the same crunch. Despite a $455bn (€392.

67bn) revenue backlog and major contracts with Meta, OpenAI, and xAI, the firm is “still waving off customers” due to capacity shortages, CEO Safra Catz confirmed. The 'backlog paradox': Contracts without capacity With CoreWeave and Oracle alone holding more than half a trillion dollars in revenue backlog, the market faces what Visser calls a “backlog paradox”.

AI firms have customers, capital and contracts, but they can’t deploy infrastructure fast enough to monetise them. Craig Shapiro, founder and managing partner of the investment firm Collaborative Fund, also raised this issue in a recent post on social media X. “AI demand collided with physical limits.

The next moat is control of land, power, water, and grid access. Firms with locked-in megawatts hold a stronger position than companies shipping GPUs. Cheap, firm power sets the pace of the entire buildout.” Bottom line, the shift underway in the AI sector is structural. This is not merely a question of whether the AI bubble will burst, as history shows that even when bubbles do collapse, the underlying technologies often resurface stronger and more transformative.

In the case of AI, the fear is not that demand will vanish — it’s that the physical world simply can’t keep up.

Source coverage

Publisher: euronews

Author: Piero Cingari

Deeper analysis

Full source content

Concerns over a potential bursting of the artificial intelligence bubble have resurfaced with intensity, as US technology stocks recently faced their sharpest pullback since the Trump tariff-induced sell-off last April. Such movements have clear consequences when the sector is so pivotal for the markets.

AI-related stocks have contributed to roughly 75% of the S&P 500’s returns, 80% of earnings growth, and 90% of capital spending growth since the launch of OpenAI’s ChatGPT in November 2022. The so-called “Magnificent Seven” — Nvidia, Microsoft, Apple, Alphabet, Amazon, Meta Platforms, and Tesla — now collectively command a market capitalisation greater than the Chinese economy.

Nvidia alone is worth more than Japan, the world's third largest economy. But first: what defines a financial bubble? Can we really say that the current AI boom qualifies as a bubble? What does this phase of market euphoria have in common with the early 2000s — and more importantly, what sets it apart?

Are current trends echoing the dot-com bubble? The investment community remains starkly divided over whether we are witnessing a speculative bubble in the AI industry. While some observers draw uncomfortable parallels with the dot-com crash of the early 2000s, others argue that the current AI revolution is underpinned by genuine, transformative economic fundamentals.

UBS chief global equity strategist Andrew Garthwaite argues that the AI boom checks all the boxes for a classic bubble. He highlights several familiar patterns. Firstly, a pervasive “buy the dip” mentality, when investors flock to an asset when its price falls. Secondly, an investor belief that “this time must be different” due to revolutionary technology.

Thirdly, increased retail participation, along with loose monetary conditions and a backdrop of stagnant earnings outside of the top ten US companies. Garthwaite notes that 21% of US households now own individual stocks, with that number rising to 33% including investment funds. Meanwhile, earnings growth is largely confined to the tech giants.

“Today, outside the top ten companies in the US, 12-month forward earnings per share growth is close to zero,” he said. However, others caution against simplistic comparisons with the dot-com era. Goldman Sachs equity analyst Peter Oppenheimer points out, that unlike speculative companies of the early 2000s, today’s AI giants are delivering real profits.

“While AI stock prices have appreciated strongly, this has been matched by sustained earnings growth, not mere speculation,” said Oppenheimer. The current scenario of expensive equity valuations, Oppenheimer highlights, is less about speculative mania and more a reflection of broader macroeconomic conditions: low interest rates, high global savings, and a long economic cycle boosting risk assets.

A key distinction between the current AI boom and the dot-com bubble of the late 1990s lies in valuations. Goldman Sachs indicates that the median 24-month forward price-to-earnings (P/E) ratio for today’s ‘Magnificent Seven’ stands at 27 times earnings. This is nearly half the median valuation of the top tech stocks during the 2000 bubble, when companies like Cisco Systems, IBM, Oracle, Lucent Technologies, traded at eye-watering P/E multiples.

Not an AI bubble, but a power bottleneck? Whether or not the AI boom will end in a bubble remains an open question that continues to divide the investment community. However, beyond speculation about future valuations, a more grounded and pressing issue is emerging. Until now, much of the conversation around AI has focused on demand— on whether AI products and services meet real customer needs.

But a new perspective is gaining traction: demand is not the problem. In fact, it is so strong that the industry’s ability to supply the necessary computing power and physical capacity is struggling to keep up. According to Jordi Visser, head of AI Macro Nexus Research at 22V Research, the AI industry is facing a serious supply-side challenge — particularly in terms of the energy and infrastructure required to support its growth.

“This is not the dot-com bubble, because demand is massively outpacing supply,” Visser said in a recent YouTube video. According to Visser, “the next AI investment phase will not be defined by who can spend the most, but by who can execute through constraint”. He cited CoreWeave’s recent earnings call as a watershed moment.

Despite surging demand, the AI-cloud company’s revenue backlog nearly doubled quarter-over-quarter to $55.6 billion (€47.98bn), CoreWeave slashed its 2025 capital expenditure guidance by up to 40%, citing delayed power infrastructure delivery. Oracle, too, is experiencing the same crunch. Despite a $455bn (€392.

67bn) revenue backlog and major contracts with Meta, OpenAI, and xAI, the firm is “still waving off customers” due to capacity shortages, CEO Safra Catz confirmed. The 'backlog paradox': Contracts without capacity With CoreWeave and Oracle alone holding more than half a trillion dollars in revenue backlog, the market faces what Visser calls a “backlog paradox”.

AI firms have customers, capital and contracts, but they can’t deploy infrastructure fast enough to monetise them. Craig Shapiro, founder and managing partner of the investment firm Collaborative Fund, also raised this issue in a recent post on social media X. “AI demand collided with physical limits.

The next moat is control of land, power, water, and grid access. Firms with locked-in megawatts hold a stronger position than companies shipping GPUs. Cheap, firm power sets the pace of the entire buildout.” Bottom line, the shift underway in the AI sector is structural. This is not merely a question of whether the AI bubble will burst, as history shows that even when bubbles do collapse, the underlying technologies often resurface stronger and more transformative.

In the case of AI, the fear is not that demand will vanish — it’s that the physical world simply can’t keep up.

How this page is built

Goose Pod turns cited reporting into a public episode summary first, then pairs that summary with audio playback so listeners can check the source material before they decide how deeply to engage.

The goal is to make this page useful as a news landing page first, while still giving listeners transcript access, related episodes, and direct links back to the original publishers.